Who would benefit from this post? Share here:

Personal finance is 1% knowledge, 1% numbers and 98% psychology.

Unless you keep all your money in ready cash or gold bars (not recommended), you can’t see it or touch it. So your mind is free to ignore your big stinking pile of debt or to focus on ice cream instead of investing your salary.

I believe I have found a way for people living at home and abroad to save and invest cheaply, flexibly and easily. You’d be surprised how hard it is to find this out, as the financial industry doesn’t benefit from telling you about it. But it’s definitely doable and here’s a 10-step plan.

So all that remains is to get your psychology handled. This is simple, but not easy. You have to train your brain to accept that yes, you will become great with money, you will stick to the path and you won’t let your monkey mind get in the way.

First, know thyself

To become a good long-term investor, you must first understand yourself and then transform your feverish financial mind into a cool, rational money processor. Mostly that involves following a few simple rules and then ignoring everything else, including your own thoughts and fears. Remember, don’t believe everything you think.

Your current approach to spending, saving and investing will come from:

- Your parents, significant other, friends and advisors

- What you choose to read

- Your beliefs about your abilities and the sort of person you are

- What worked well or badly for you in the past

- What sort of economic booms and crashes you have lived through

Most of what you have heard, thought and done financially has probably been wrong. Or at least, not ideal. Don’t feel bad though, we’ve all been there. It’s a form of education – after all we don’t get taught this stuff at school.

Forgetting years of bad advice

There’s a lot of bad advice out there – you shouldn’t have believed that smooth-talking chap or that catchy article. You shouldn’t have bought one stock your Dad recommended and then avoided the rest of the stock market because the economy might crash.

Put your cynical hat on and trust nobody except yourself. Don’t trust what I say until it makes logical sense to you.

It’s best to accept that most people don’t really have a clue about finance and are just recommending what kinda worked for them, in their own circumstances. Commission-driven financial advisors, banks, stockbrokers, fund managers and newspapers (reliant on advertising from the others) are not going to give you simple, impartial advice. They want you to buy their complicated, expensive stuff, sell it and then buy something else.

If you want some safe havens of knowledge you can trust, I recommend: this website :), googling blogs under “financial independence”, the Bogleheads (based on the wisdom of Vanguard founder Jack Bogle, the books and blog of Andrew Hallam (the Millionaire Teacher), the facebook group SimplyFI and hmmm that’s about it for now.

Googling ‘personal finance’ or ‘stock market investing’ is more likely to yield some ugly stuff best avoided.

Reshaping who you are

You may believe you are destined to always be bad with money, terrified of maths and better off letting someone else deal with your finances. You may have seen others wrecked in the great crash of 2008 or been hurt financially yourself.

You may see yourself trapped in a job you don’t love, possibly forever, with mounting debt and little to show for your hard work. You may feel retirement is a myth – by then social security and the stock market will have collapsed, and the robots will take over anyway.

The entire purpose of this site is to show you that you can save money, get out of debt, build a fast-growing retirement portfolio and live comfortably and securely. If your boss is a jackass, you can get another job, or perhaps never ‘work’ again.

You must believe this is possible. If you are struggling, explore the fantasy anyway. What would it feel like to be financially independent? What kind of life would you live? Think hard and imagine the details. Now, what are five things that you could do (or avoid) to move a little bit closer to that fantasy this year? Maybe it’s not so fantastical after all.

Resolve to become that person. Find people who have achieved financial independence and understand what they did – find the ones closest to your current situation and beliefs.

By the way, you probably aren’t as bad with numbers as you think – at most we’re dealing here with adding and some percentages. I believe that anybody can figure out the basic arithmetic to manage their personal finances properly and safely. There are plenty of templates and tools to help you with expense tracking or compound interest.

Managing the tribe

Your brain is like a tribe of people with different goals and opinions. One simplistic part might say “Yes! Ice cream!”, while another part says “No, you are on a diet.” and a more sophisticated part says “Well, I did diet all week so maybe I can cheat a bit if I only have two scoops.” Your behaviour can be quite different depending on which part of your brain is dominant at the time.

You’re going to have to learn to listen to your financial tribe (I’m curious about Bitcoin!), filter out the noise (Bitcoin could make me lots of money!), stick to the rules (Bitcoin is super risky!) but also know when to give yourself a break (alright, I’m allowed to gamble 1% of my investment portfolio on Bitcoin).

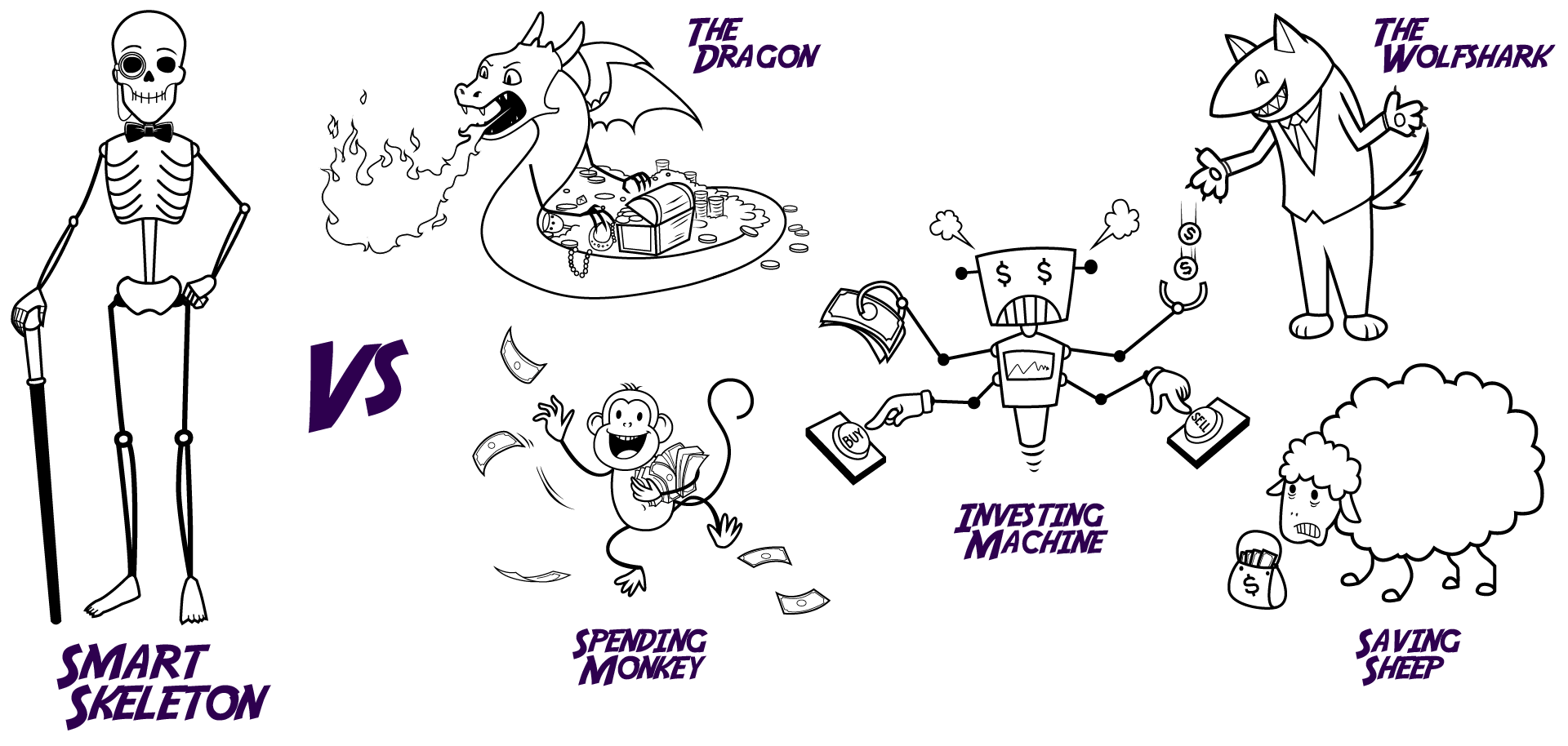

Investing personalities - a bad day at the zoo

It helps to recognise some common investing personality types, mostly so you can avoid them. Which of these do you recognise in yourself? I’ve added some tips on how to handle that part of your personality.

The Spending Monkey

Reducing your expenses will boost your saving rate and accelerate your journey to financial independence (don’t forget to try to grow your income as well). Are you able to squirrel away 10% of your salary every month? Ideally, you should be looking at 50% – and some people even manage 80%. Push your saving rate as high as you can sustainably – you don’t want to be miserable or get scurvy from eating only potatoes.

You’ll be fighting against years of advertising that have trained our brains to be consumers. Apparently, consuming = happiness. So when you are feeling down, or walking past your favourite shop, the little Spending Monkey in your head gets excited.

Don’t be surprised if you find yourself clutching a new phone, new bag or even an avocado in your sweaty paws.

How to defend yourself against the Spending Monkey:

- In a shop, realise you are about to make an unnecessary purchase and shout “Monkey NO!”. Sheer embarrassment should force you to leave the shop, with your wallet intact

- Track your main expenses and, if that isn’t sufficient to halt your spending, set yourself a monthly budget for each expense category, including luxury (i.e. non-essential) items

- Spend money on experiences rather than objects – that way you can enjoy planning, experiencing and remembering them

- Learn to say no to peer pressure (do you need new peers?) and take advantage of the endless two-for-one and discount deals available these days

- Learn to enjoy saving, so the satisfaction of hitting your target saving rate is greater than the brief pleasure from spending. Think of all the great things you can do when you hit your net worth target – remember $500 saved now will likely be worth $5,000 in 30 years!

Make sure you also avoid the monkey’s loser friends: Keeping Up with the Joneses Giraffe, Shiny Object Magpie, No-Self-Control Salamander and Down in the Dumps Donkey.

The Dragon

Many people love to sleep on their pile of treasure, where they can touch it and protect it. They feel comforted by all the zeros in their bank balance. Property is also something real, solid and tangible.

You had better have a fire-proof suit on before you recommend investing in the stock market, because you’re going to get burned! To the risk-averse dragon, the stock market is for gamblers – a high stakes game where your money could disappear at the roll of dice.

Dragons crave safety, stability and predictability for their money, especially if it is linked to their children. Unfortunately, this is not a good approach for retirement investing, or even education investing, over 10 to 30 years.

The inflation monster will relentlessly eat around 3% of your cash savings every year, which turns into 20% of your cash over 10 years. You must take some (sensible) risk to out-run inflation.

How to reduce your Dragon-like tendencies:

- Check what 3% of your total cash balance is worth. I bet you could buy something nice with that, so don’t let inflation take it!

- Learn how to track your net worth and manage your income, expenses and investments. It is this discipline that gives you control and resilience, not having lots of cash for a rainy lifetime

- Learn about the pitfalls of real estate investing, such as high ongoing costs, difficulty in pulling your money out quickly (illiquidity) and annoying tenants. Then at least you’ll invest with your eyes open

- Face your fear of the stock market by learning how to invest cheaply in diversified stock and bond funds, so that you can build an inflation-proof retirement portfolio without taking unnecessary risk over the long term

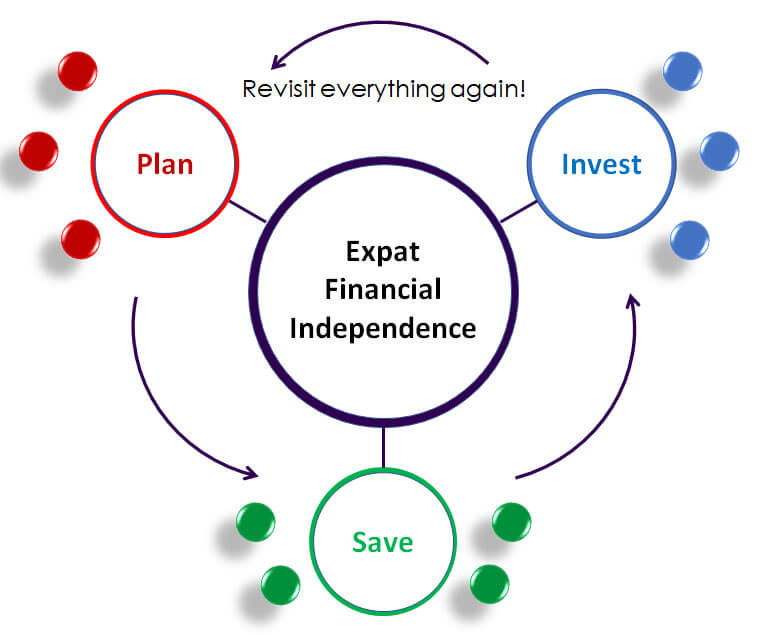

Get started with my free guide:

3 Steps to Expat Financial Independence

15-minute read. Discover the simple process for taking control of your finances so you never have to stress about money again.

The Saving Sheep

The poor little Saving Sheep knows it should invest its money but doesn’t know where or why. So it usually finds itself at the mercy of the Wolfshark (see below), or following out-dated advice from parents, or jumping on the bandwagon of the last article it read.

Dragons can be held back by the thought of turning into a Sheep – imagine having to tell people you invested all your cash and gold in something you barely understand!

Education and discipline are the only ways to escape from woolly thinking. There’s a lot of bad advice out there and unfortunately, there are a lot of bad things to invest in, ranging from sub-optimal to completely toxic.

Make sure you can justify every investing step you take. Don’t get frozen though and do nothing for 6 months while you read everything available. The conflicting advice might make your head explode. Investing even a small amount of money now, in the cheap and flexible way we suggest, will train you up to become a long-term investing badass

How to stop being a Saving Sheep:

- Learn about financial independence and the steps to get there –see the blogs and books mentioned above – but take action and don’t get paralysed by too much information

- Try to progress through the steps to financial independence as quickly as possible, training yourself up on investing even if you are at the debt reduction stage

- Do not believe anybody when it comes to investing, even me. Develop your own opinion and assess everyone’s motivation for giving you specific advice. If you can’t explain it, don’t do it!

- Always make sure the core of your portfolio is invested in solid assets like stocks, bonds and property. Keep your investments cheap, simple, diversified and easily accessible

- Never invest in anything that promises you more than 10% return per year, it is almost guaranteed to be a scam

If my advice is getting a bit repetitive, remember personal finance is all about psychology. Unfortunately, your brain really needs a good hammering – they didn’t have stocks where our ancestors came from.

The Wolfshark

Many people decide to do something about their finances and then walk straight into the jaws of a Wolfshark. It doesn’t matter if their website is slick, if you got a referral from a friend, if the advisor is your cousin or if four different advisors all tell you the same thing. I have heard sad stories from all of these situations.

The Wolfshark may have a big smile and pretend to be your friend, but he (or she) is not on your side. Behind the smile they are usually full of greed, ignorance and fear, none of which are going to help you. Greed for the big commission bonuses advisors can get for selling you terrible products. Ignorance because they are usually salespeople with little financial experience, who often follow their own terrible advice. Fear for the trouble they’re going to get into if they don’t hit their sales targets.

Beware well-known brands that can lull you into a false sense of security. For example, it’s safe to say nobody at a bank is going to give you good, impartial advice, especially if you are an expat.

Banks are set up to make money from you at every turn, often without you really noticing. Nearly everyone trusts their bank as a place to deposit money, which is reasonable enough. Unfortunately, they then extend that trust to taking investing advice. Bank advice isn’t going to be terrible, but it’s rarely going to be excellent. They have to pay for the staff bonuses somehow.

To truly vaccinate yourself against the money-eating viruses that Wolfsharks spread:

- Learn enough about cheap, flexible and diversified investing, as well as potential scams, to call people out on their bad advice

- Never, ever trust the recommendations of someone receiving commission for a product they recommend – assess how each company involved is making their money

- Check the internet before you buy a product from any financial advisor – read up on both the product and the advisor, e.g. googling avoid [name] to discover any negative views

- If you really don’t trust yourself to invest sensibly (and you should), find a financial advisor who charges a fixed fee for advice or a (hopefully small) percentage of your invested assets

- Avoid investing in a product or service that costs you more than 1% in fees per year, or that you can’t get out off without a surrender penalty

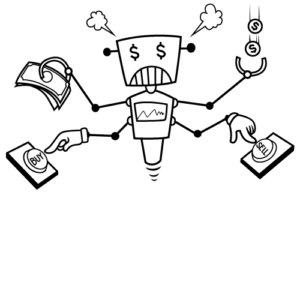

The Investing Machine

When investing, a little bit of knowledge (or even a lot of knowledge) can be a terrible thing when mixed with over-confidence. Swaggering Sheep can easily turn into Investing Machines. Brokers, fund managers and advisors will all encourage excessive activity and complexity, as it makes them money. Some examples from my friends:

- Desperately trying to unwind your death-spiralling portfolio of options, while your wife impatiently waits outside to go to a dinner party

- Feeling smart with your big Florida house mortgage in Swiss francs, until the housing market collapses (asset value goes down) while the franc strengthens against your feeble pounds (mortgage liabilities go up, ouch)

- Losing all your many years of day-trading profits in one bad year (then sensibly switching to passive index trackers)

- Financial advisors constantly ‘churning’ your money into new funds until there isn’t much left

When you think of the stock market, you probably think of traders. Stressed people shouting on the trading floor or sweating into their screens as they buy and sell every two minutes. Do not confuse this type of gambling with the much less risky practice of buying and holding a diversified portfolio of stocks.

Trading has the same allure as bitcoin – a way to make lots of money with plenty of adrenaline and a bit of smart timing. It reels you in, just like a casino: a successful trade, maybe a good week, even a good year. But in the end, nearly everyone ends up down. A bad trade cancels out the 6 previous good trades, a bad year cancels out the previous 6 good years.

Do you really want to base your future on that kind of stress? Nope. At DeadSimpleSaving, we like to spend at most one hour per year thinking about our portfolio, then spend the rest of our time doing much more interesting things.

How to avoid being an Investing Machine:

- Never invest in something that you couldn’t explain simply to your grandmother

- Avoid all courses on trading – stocks, foreign exchange, options, commodities, cryptocurrencies – and avoid any company that offers to trade on your behalf

- Avoid any kind of active fund or individual stock for your core portfolio (i.e. 90% of your net worth) until you have been investing for at least 5 years – stick to passive index trackers

- Only invest your core portfolio in assets you intend to hold for at least 10 years

The Smart Skeleton

You may now be thinking this is all too much – there are so many pitfalls, so much to learn, so much risk, it’s just too hard. Yes, finance can be extremely complex and you can lose your shirt.

But there is a narrow path that cuts through the dark financial forest. Let’s call it The Way of the Smart Skeleton. It’s an approach that is straightforward, logical and backed by scientific studies. And it really is dead simple.

Your brain will try to mess up your investing at every turn. You will want to check the value of your funds every day and beat yourself up when the value goes down an hour after you invested. You will wonder if you invested in the right funds. You will want to yank your money out of the market when the papers say there might be a crash. Your friend will tell you about a great investment opportunity and exactly how you are missing out by being so passive.

You must resist all these temptations. The best way to do this is to imagine you are dead.

A skeleton has limited investment options. You can’t track the markets, read the financial news, fret about a downturn or get distracted by new opportunities. All you can do is stick to whatever you laid down in your ‘will’, i.e. your investment plan.

When you start worrying about your investments, think: “What would a dead person do?” Certainly, those who kept their money invested during the crashes of 2008 and 2020 are now significantly better off than those who pulled their money out.

You need a specific investing method to be able to invest so rigidly. You should put your long-term investment money in cheap, highly-diversified, passive index funds, with an appropriate mix of stocks and bonds. Every month or every quarter, you invest in the same funds and maintain the same overall stock and bond mix, not worrying about what the market is doing.

Epilogue

This may feel like it’s too simple and you should be working hard for your investment gains, or getting regular advice from someone wonderfully experienced and clever. It’s just not true.

The Way of the Smart Skeleton doesn’t take up much time or brain power. This frees up both to live a fantastic life, happy in the knowledge that you are building a retirement portfolio in the most efficient way possible.

Don’t forget to wave at all the monkeys, dragons and sheep on your way past. Wait… maybe you can stop and help them out, given all the free time you have now.

Who would benefit from this post? Share here:

Hi there, as I am not a US citizen I cannot open a Vanguard account. What local brokers can you recommend that will give me access to Vanguard index funds? Thanks

Hi Nathalie, people typically use Interactive Brokers or Saxo Bank among others, as discussed further here: http://www.deadsimplesaving.com/blog/guide-offshore-investing-expat-etf/

Hi

Thanks a lot for sharing your knowledge and insights – I found your website very easy to understand and I feel more confident in my investment plans.

I have a specific situation that I believe you can best advise me on: I was a UAE resident, and will be moving with my company to London for 2 years. So I suppose you can say I would be a UK resident for 2 years according to my visa, which can be extended up to 5 years.

Having read your website, it seems that it’s best for me to transfer my money to a UK bank account and directly invest in Vanguard. My only concern would have been exchanging AEDs to pounds during this period (Brexit!). Do you recommend this? Second question: would you know whether I would have to stop my investment with Vanguard if I were to stop being a UK resident after 2 or more years?

Thanks!

Are you a UK citizen? If you are only planning to be resident there for two years, you could keep your current investments with your brokerage (e.g. Interactive Brokers), invest new money in an ISA in the UK in Vanguard LifeStrategy tax-free, then on leaving either leave it there growing tax free or closed it and merge it back with your other brokerage account.

I came across this site when I read an article on a newspaper. I find this very informative, along with the funny mix of characters.

Do you currently have local investments in the UAE or maybe recommend some? All of my investments are back home (stocks & mutual funds) and am trying to diversify my portfolio, if I can, while am in Dubai.

Thanks! I don’t really recommend investing in the local stock markets, as they are very volatile, unless it is ‘fun money’ that is less than 10% of your net worth. It’s much better to get global exposure via a highly-diversified ETF such as VWRD.

Hi !

Great blog ! I have a question for you, correct me if i am wrong, that you are converting your money in USD before investing via an online broker to vanguard etf (or other ETF).

I am lookong into investing my AUD in EUR to some ETF as it is the most likely place where we will move in the next couple of years,but it seems to be a lot of fees as you add the currency change fee to a normal direct investment no ? Wouldn’t that represent a significant amount of money on the long run ?

Hi Loic, yes I convert AED into USD and then send to my broker. There are always lots of debates around currency conversions. If you are investing in a globally-diversified stock ETF like VWRD then the underlying currency of most companies will be USD. It doesn’t then really matter which currency you invest in. Check what currency the dividends would be paid in. Maybe invest in AUD ETFs now and then EUR ETFs when you move. The same cannot be said for bond ETFs, which are affected by the currency you invest in. For these, maybe consider 50-100% of your bond allocation in EUR (can still be global bonds but hedged to EUR).

This is great. 2 Questions:

1) Can you tell us which online broker you recommend to use and why?

2) Can you give us some examples of “cheap, highly-diversified, passive index funds, with an appropriate mix of stocks and bonds”?

Hi Ped, glad you like this article. I use Interactive Brokers in the US, because they are cheap, large and reputable. For funds I would recommend ETFs such as VWRD, the Vanguard FTSE All-World UCITS USD fund, which covers a very diversified pool of international stocks. Bond funds such as IAAA or IGLO are similarly good.